A watch-list, a special servicing event, and maximizing NPV recovery all have this in common

Question: “What is a landlord with a troubled CMBS loan?”

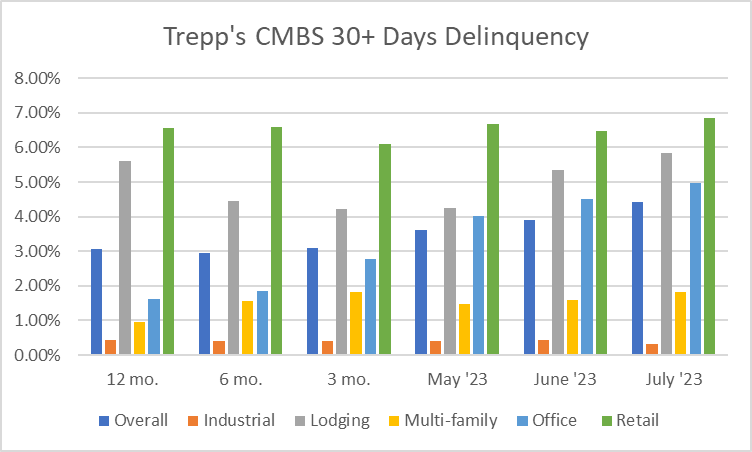

Given the 12-month spike in CMBS loan office building defaults from 1.62% to 4.96% as of July 2023, we have updated this blog which Terry Beal originally posted in 2011.

Back in the day, a landlord may have had a loan with a life insurance company in Iowa or a pension fund in California that retained the loan through maturity.

Then, smart money came along and structured a secondary market for the trading of commercial mortgage-backed securities (CMBS).

Now, mortgage bankers can transfer loans to a tax-advantaged trust. The trustee, with promissory notes in hand and an expectation of receiving regular interest payments on the pool of loans, can issue a series of bonds varying in yield and risk. Rating agencies can come in and assign ratings to the various bond classes: from the most secure AAA down to the below-investment grade and unrated bonds. Bankers can underwrite and sell the securities to investors. Bond investors can select from the tranche matching their credit risk, yield, and term preferences. Meanwhile, down in the boiler-room, a master servicer, engaged by the trustee to service the loans, would collect mortgage payments, release disbursements from escrow, and handle other routine loan matters, all so long as a loan performs as expected.

However, we first saw a wheel or two come off the truck during the 2008 recession (which is repeating itself this year), where some loans have not performed as expected. Unlike the recession 15 years ago, today the economy is healthy, but interest and vacancy rates are at record highs as the demand for office space is not returning to pre-pandemic levels given hybrid and remote work models.

According to data provider Trepp, approximately $1.5 Trillion in commercial mortgages are maturing in the next 3 years. Trepp indicates that 88% of these CMBS loans are interest only compared to 51% in 2013. When times were good with cheap debt and rising property valuations, landlords would pay off these interest-only loans by refinancing or selling the building. According to CoStar, 83% of today’s outstanding CMBS office loans cannot be refinanced at current rates. As most of these loans are non-recourse, the landlords, who are upside down on these buildings, are more inclined to turn the keys back to the lender.

Watch-list, Special Servicing Event, and Maximizing NPV Recovery

When crossing paths with a landlord with a troubled CMBS loan, the following terms/concepts may be part of the story:

Watch-list: A list of “at-risk” loans monitored by the master servicer. A loan could be put on the watch-list because an anchor tenant’s lease is rolling, the building’s occupancy level has declined, the Debt Service Coverage Ratio is below the threshold required by the loan documents, or perhaps the loan is simply approaching maturity.

Special servicing event: Usually a monetary or maturity default on the loan, triggering the transfer of the loan servicing responsibilities to a special servicer. The special servicer is appointed by the first-loss bondholder(s) and, in fact, is often an affiliate of the first-loss investor.

Maximizing NPV recovery: The special servicer is mandated to maximize the NPV of the bondholders’ recovery when evaluating alternatives. These alternatives include restructuring the loan, a negotiated payoff, a sale of the defaulted loan, foreclosure, and a deed-in-lieu of foreclosure.

What’s a tenant to do?

While undoubtedly the prudent tenant will have done its homework in evaluating a prospective landlord, the future is nonetheless unknowable. A longstanding anchor tenant may go bankrupt. A seemingly solid landlord may be unable to refinance its loan. A global pandemic may come along and disrupt how businesses use office space.

Consequently, the prudent tenant will also have worked during negotiations to protect its interests in case of lender foreclosure as well as against a landlord’s monetary default or failure to perform under the lease. In such cases, the SNDA language, self-help rights, set-off rights, termination rights, escrow and LOC requirements contained in the lease are no longer mere boilerplate, but key rights.

Existing tenants and their tenant representatives should monitor the building and the public disclosures that are required to be made as to the status of CMBS debt. To read the tea leaves, it would also be wise to monitor other buildings that the landlord owns as landlords frequently cross-collateralize CMBS debt across multiple properties in their portfolio. Where a tenant is planning to have its landlord fund any improvements, etc., having those funds placed in escrow is wise. Tenants (including existing) must be aware that many lease commitments will require lender consent and, to avoid negotiating in a vacuum, a prudent tenant will obtain the lender’s consent during negotiations and before finalizing any document. During the CMBS default process, existing tenants will receive an estoppel certificate from the CMBS servicer. As we wrote about in What Tenants Need to Know About Estoppel Certificates – Blackacre Advisors, estoppel certificates are critically important documents that can alter a tenant’s lease if not timely and properly reviewed.

The prudent tenant will also recognize that the special servicer’s directive to maximize NPV recovery might present the well-positioned credit tenant with an opportunity to improve its deal. This opportunity stems from the fact that any refinancing of the loan or any sale of the property will be predicated on the value of the property. The credit tenant whose rent payments account for a meaningful percentage of the property’s cash-flow may find that it has some cards to play.

Don Wenig

Blackacre Advisors LLC

info@blackacreadvisors.com

312-345-4778

DISCLAIMER. Our writings are from a real estate transaction perspective and for informational purposes only. Nothing herein shall be considered legal, accounting, tax, or architectural advice. Please consult with the appropriate professional(s).